Carve-Outs, Spin-Offs, and Divestitures Shaping the Future of M&A

Mergers and acquisitions, a staple in the business world, represent the consolidation of companies or assets, often aiming to achieve growth, enter new markets, or

Blog Webinar Recap: How to Value Small and Medium Enterprises

SHARE:

In the Institute for Mergers Acquisitions and Alliances’ webinar on How to Value Small & Medium Enterprises, experts from Valutico – Greg Brown, Alex Harris, and Max Lahrmann – delved into the pivotal role of small and medium-sized enterprises (SMEs) in fostering economic growth and sparking innovation. The discussion brought to light the unique challenges and methodologies in valuing these vital yet often overlooked components of the economy. Continue reading to learn about the key takeaways from the webinar, including why SME valuation is essential, the discrepancies between theory and practice, and specific considerations unique to SMEs.

The webinar highlighted several key reasons why valuations are crucial for small and medium enterprises (SMEs), noting that these businesses differ significantly from larger, publicly traded companies. Here are the main points:

These reasons, while sometimes overlapping with those of larger companies, are particularly pertinent for SMEs and are a daily aspect of the world of valuation.

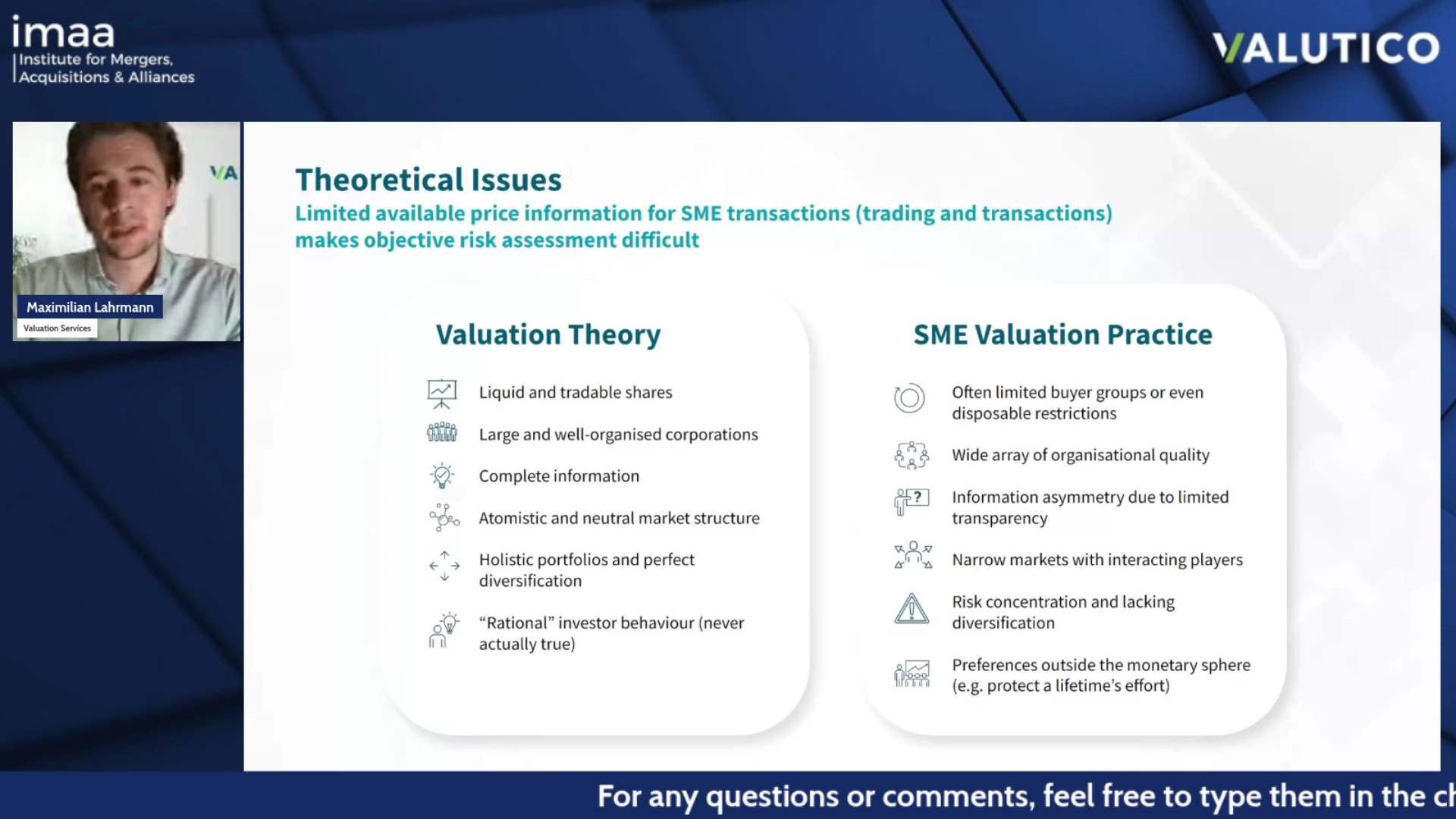

The webinar delved into the noticeable discrepancies between traditional valuation theories and their application to small and medium enterprises (SMEs). The key points discussed were:

The session highlighted that while traditional valuation models provide a foundation, applying them to SMEs requires consideration of these unique factors.

The webinar explored distinct characteristics of small and medium – sized enterprises (SMEs), highlighting how these differ from larger companies and significantly influence their valuation. Understanding these specifics is key in accurately assessing the value of an SME. The discussion was segmented into three primary areas: Organization and Management, Financial and Legal Aspects, and Reporting and Planning.

The webinar highlighted the unique aspects of organization and management within SMEs, which differ significantly from larger companies. These differences impact the valuation of SMEs in several ways:

The webinar also covered the financial and legal peculiarities of SMEs, which play a crucial role in their valuation. These aspects are often distinct from what is observed in larger enterprises:

Focusing on reporting and planning, the webinar addressed how these processes in SMEs are often distinctly different from those in larger companies, impacting their valuation:

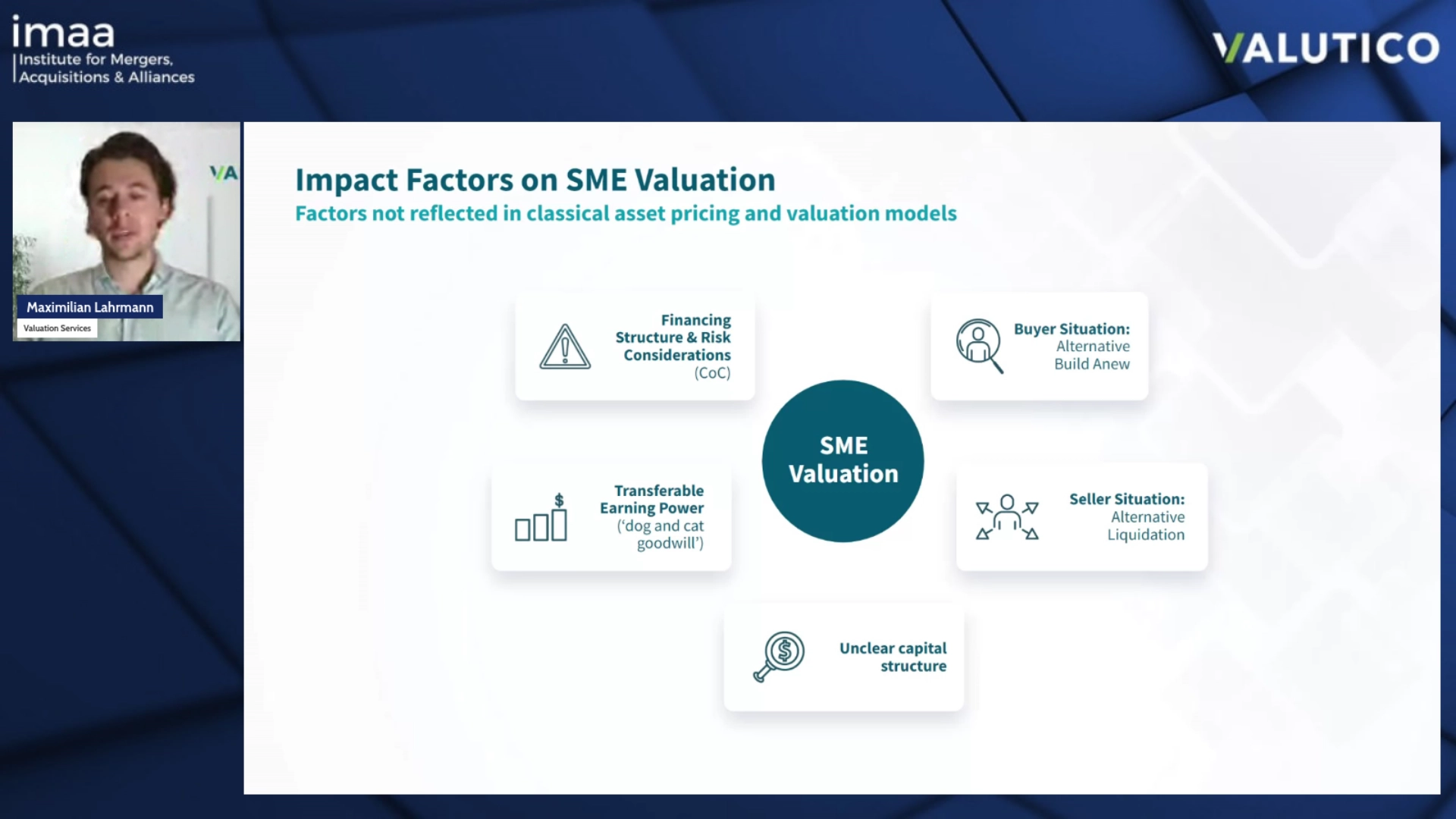

The webinar provided key insights into the practical challenges and factors impacting the valuation of SMEs. Here are the points discussed:

These factors collectively underline the complexity and unique challenges in SME valuation, emphasizing the need for tailored approaches and careful consideration of these distinct aspects.

The webinar contrasted theoretical valuation models with practical approaches in the context of SMEs, highlighting several key differences:

In summary, while theoretical valuation models provide a structured framework, the practical valuation of SMEs requires navigating a more complex and less predictable landscape, with emotional, organizational, and market factors playing significant roles.

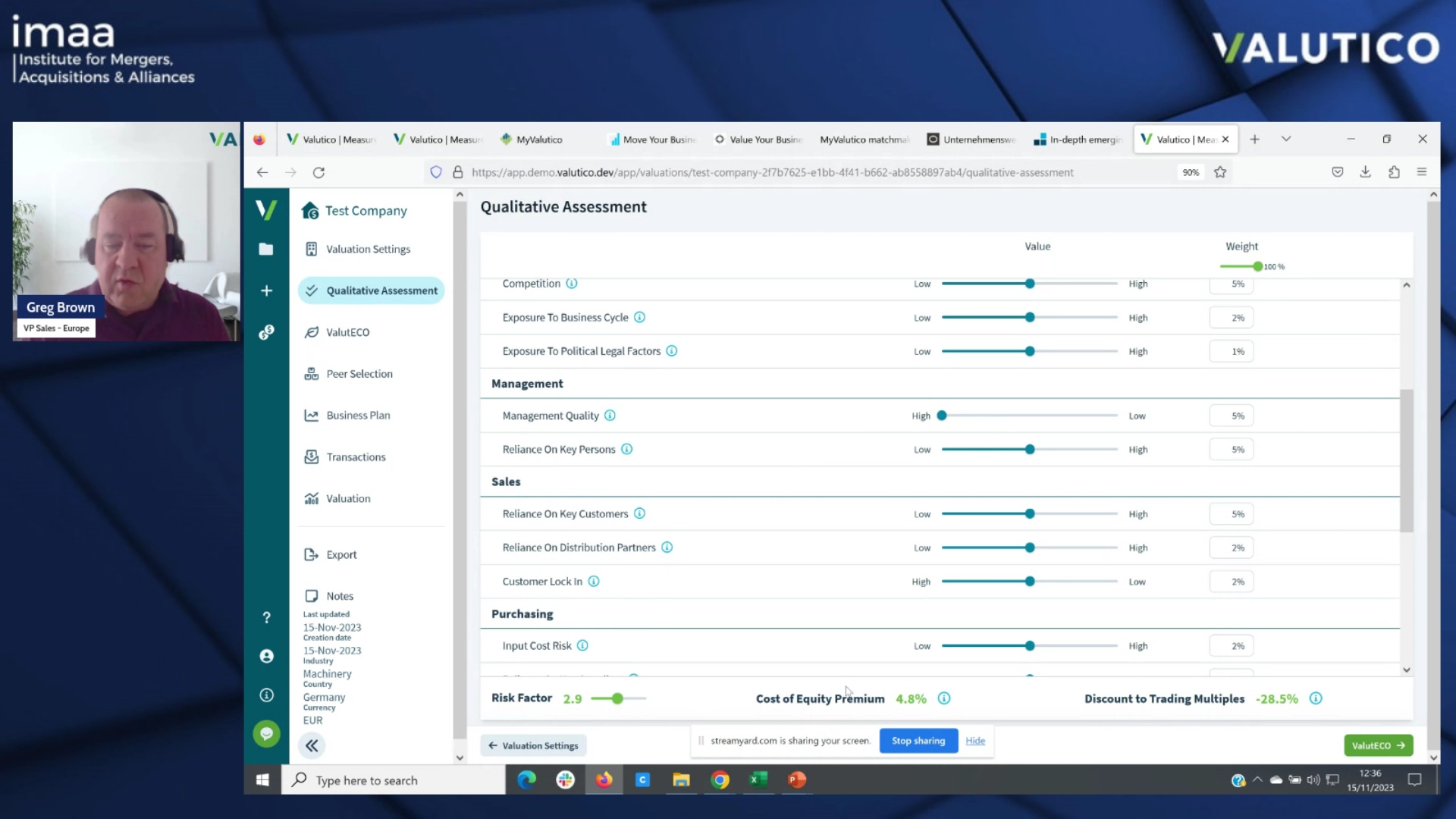

A practical case study was also presented during the webinar illustrating the application of SME valuation theories and methodologies in a real-world context. This case study focused on valuing a machinery company, utilizing the advanced capabilities of Valutico’s cloud-based valuation platform. The demonstration provided a step-by-step guide on how to leverage the software for comprehensive SME valuation, underscoring the blend of theory and practice in the valuation process.

The valuation process using Valutico’s software involves several key steps:

The case study provides key insights into the practical aspects of using advanced valuation software for SMEs. It emphasizes the need for a comprehensive understanding of both qualitative and quantitative factors influencing SME valuation. The insights highlight the software’s flexibility and depth, showcasing how technological integration can streamline the valuation process while ensuring accuracy and offering diverse customization options.

To fully grasp the intricacies of valuing an SME using this software, it’s highly recommended to watch the full webinar. The webinar not only demonstrates the valuation process step by step but also provides insights into how to navigate the platform effectively. It’s a valuable resource for anyone interested in SME valuation, offering a practical perspective that complements theoretical knowledge.

The webinar concluded with a Q&A. Below are the questions and their summarized responses:

Answer: The approach to narrowing down the peer group involves focusing first on operations to find peers operating in the same area, which is crucial for valuation. The second aspect is considering the geographical market, as it significantly influences profitability and market structure. If these criteria are met, further refinement can be done by looking for smaller cap companies if valuing a smaller company and using keyword research to identify unique aspects of the company.

Answer: For valuing a loss-making startup, the Venture Capital (VC) method is usually used. This method is specifically designed for valuing startups, particularly effective in scenarios of loss-making and fast-growing companies. It involves seeking an exit of the investment at a future date at a price consistent with valuation multiples observable in the markets.

Answer: When valuing SMEs in the current market, it’s important to do extensive market research, particularly focusing on the cost of capital. This includes monitoring operational market trends such as the number of M&A transactions in a specific market and economic factors like the risk-free rate and market risk premiums. These factors influence the markets and are crucial for an accurate valuation.

The webinar on the valuation of small and medium-sized enterprises (SMEs) provided essential insights into valuing small and medium enterprises, differentiating these processes from those used for larger companies. Key topics covered included the importance of SME valuation for transactions, financial reporting, and company succession. The discussion highlighted the need for a tailored approach in SME valuation, addressing unique challenges such as owner involvement and specific financial and legal aspects. A practical case study using Valutico’s software demonstrated the application of these concepts, emphasizing the role of technology in enhancing valuation accuracy and efficiency. Overall, the webinar bridged theoretical knowledge with practical application, offering valuable perspectives for professionals in SME valuation.

Mergers and acquisitions, a staple in the business world, represent the consolidation of companies or assets, often aiming to achieve growth, enter new markets, or

IMAA’s 2024 Top Global M&A Deals industry coverage offers an overview of the year’s most significant M&A transactions across eight key industries. This monthly M&A

Explore the transformative journey that mergers and acquisitions activity is bringing to the sports industry. The Institute for Mergers, Acquisitions, and Alliances (IMAA) dataset on

Stay up to date with IMAA Institute company news

Trainings

© Institute for Mergers, Acquisitions and Alliances

In order to become a charterholder you need to complete one of the IMAA programs